![]()

In 1935, President Franklin D. Roosevelt signed into law the Social Security Act containing, among other things, provisions for Unemployment Insurance (UI) as a state-federal partnership program. UI is an important safety net program that can help ensure that workers and their families can avoid economic catastrophe following a layoff. However, Michigan has implemented policies over the years that have directly weakened this safety net, and failed to pass other policies that could have strengthened it.

MICHIGAN’S WEEKLY BENEFIT HAS ERODED OVER TIME

In 1995, the Advisory Council on Unemployment Compensation to the President and Congress recommended that state UI systems replace at least 50% of eligible workers’ lost earnings over a six month period, and that the way to do this was to set a maximum benefit equal to two-thirds (66%) of the state’s average weekly wage.1 This objective dates back to the founding of the UI system and was endorsed by President Dwight Eisenhower and most presidents thereafter. President Richard Nixon said that UI should replace 50% of lost wages for four-fifths of all UI recipients—this became known as the “one-half for four-fifths” criterion.2

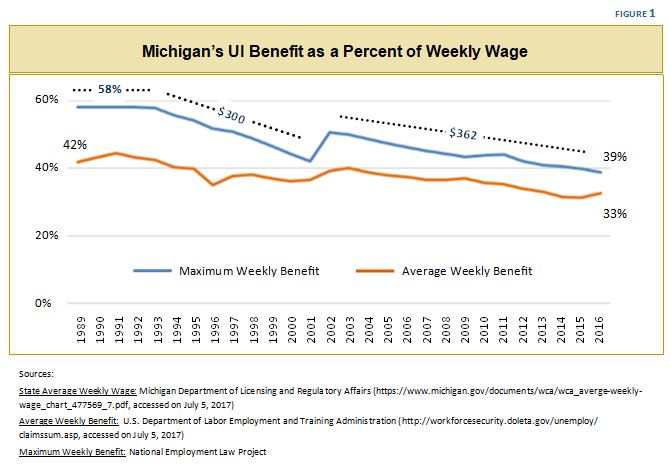

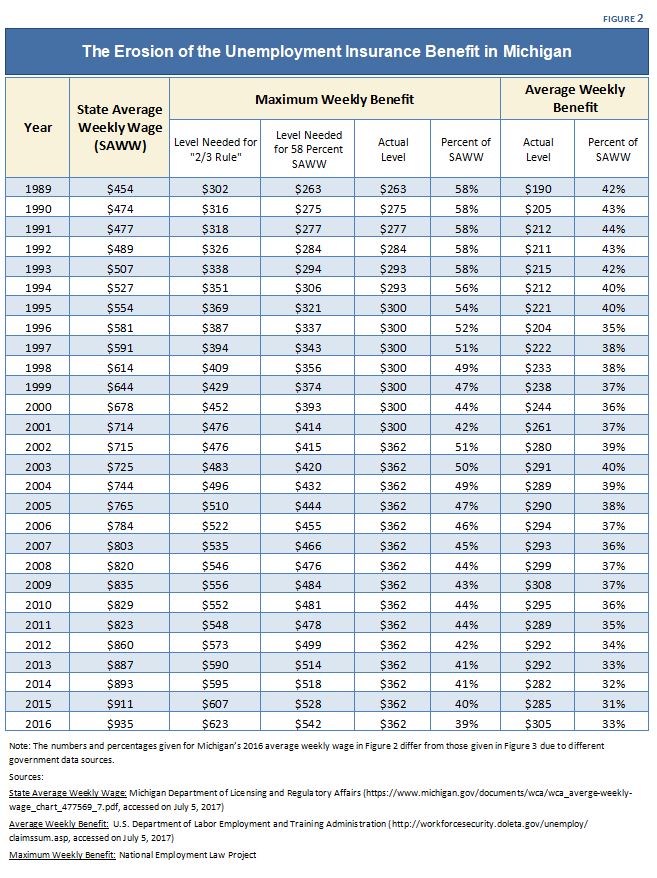

Michigan falls far short of this standard. Since 1989, the earliest year for which data are available for this report, Michigan has not met either the two-thirds standard for the maximum benefit or the 50% standard for the average weekly benefit. Until 1993, the maximum benefit was pegged at 58% of the average weekly wage, but in 1994 the maximum benefit was decoupled from average wages and set at $293 per week. The maximum has been increased two times since then: to $300 in 1995 and $362 in 2002 (Figure 1).3

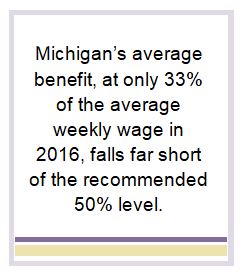

Decoupling the maximum benefit from the average weekly wage and converting it to a flat numerical amount has resulted in a significant erosion and a loss to Michigan’s workers. If Michigan had kept its maximum benefit at 58% of the average weekly wage, the maximum benefit would have been $542 per week in 2016 rather than $362. If the maximum benefit were equal to 66% of the average weekly wage, as recommended by the advisory council and most United States presidents, it would have been $623 per week. It is currently 39% of the average wage. Michigan’s average benefit, at only 33% of the average weekly wage in 2016, falls far short of the 50% level recommended by the advisory council (Figure 2).

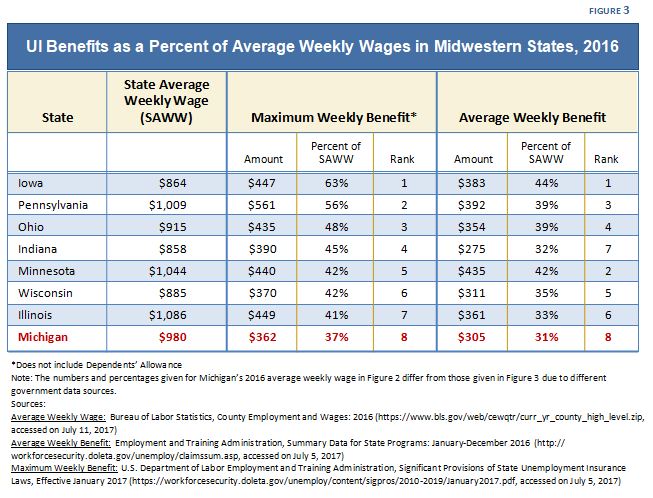

MICHIGAN PAYS THE LOWEST MAXIMUM BENEFIT IN THE MIDWEST, RESULTING IN A LOW AVERAGE BENEFIT

When compared with the other Midwestern states, Michigan’s maximum benefit ranks last, both as a nominal amount and as a percent of the state average weekly wage. During 2016, none of the eight Midwestern states had maximum benefits that met the two-thirds standard, but Michigan’s maximum was significantly below all the other states at only 37%. If Michigan had kept its maximum at 58%, as it had prior to 1994, its maximum benefit of $542 per week would rank second among the eight states. Partly as a result of Michigan’s low maximum benefit, its average weekly benefit is 31% of its average weekly wage, last among the eight states (Figure 3).

MICHIGAN’S UI BENEFIT FALLS FAR SHORT OF NEED

According to the Working Poor Families Project, nearly 310,000 (32%) working families with children are low income, meaning that their household incomes are less than two times the poverty level.4 Nearly half of these low-income working families pay more than one-third of their household income on housing, the level at which housing is considered unaffordable.5 These families likely do not have savings or other resources to deal with an unexpected job loss, and therefore, a safety net to provide for them while the unemployed parent looks for work is essential.

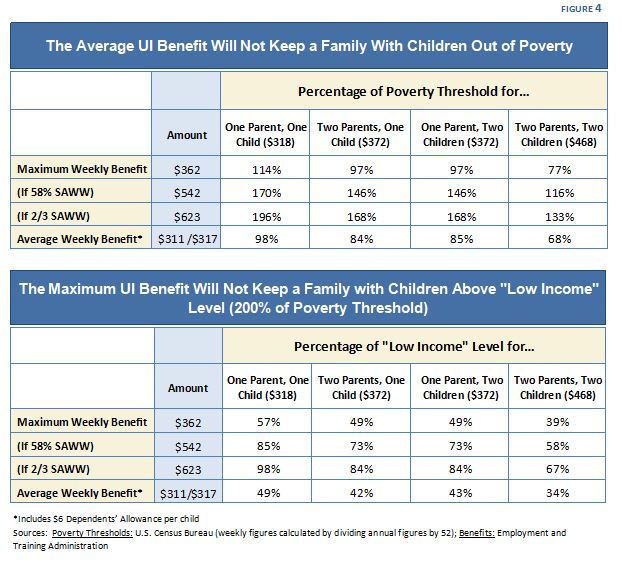

As a lifeline for workers and their families, Michigan’s Unemployment Insurance program does not keep up with economic realities. The average weekly benefit will not keep a family with children out of poverty while the unemployed parent looks for work, and the maximum weekly benefit will not keep a family with more than two people above the federal poverty level. For families in which the wages of the unemployed parent provide the only (or primary) income, this can create significant hardship.

If Michigan’s maximum weekly benefit were still pegged to 58% of the average weekly wage and if the average benefit covered 50% of wages for most workers, UI would keep the families of unemployed workers well above the poverty line as they look for jobs (Figure 4).

Many two-parent families are dual income and hence would not likely fall into poverty based on the UI benefit, but all would fall below the level considered “low income” as they look for work. Especially for the long-term unemployed, whose benefits expire after 20 weeks even if they have not yet found work, the consequences of the low benefit can be disruptive and harmful.

MICHIGAN’S DEPENDENTS’ ALLOWANCE IS OUT OF DATE

States have the option to add a dependents’ allowance to a UI recipient’s basic weekly benefit. The dependents’ allowance can be either a fixed numerical amount per dependent or one that increases with the level of the basic weekly benefit. Michigan’s dependents’ allowance is $6 per dependent. Recipients can claim up to five dependents for a maximum of $30 for the dependents’ allowance. The dependents’ allowance may not bring the total household UI benefit higher than the $362 weekly maximum benefit.

Interestingly, the dependents’ allowance in 1951 was $2 for the first dependent and a maximum of $4 for all additional dependents for a total of $6, equal to $58 today.6 The maximum weekly benefit during that year was $35, equal to $340 today, but unlike today, the dependents’ allowance in 1951 could bring the total benefit to higher than the established maximum.7,8

Michigan neglected to increase the dependents’ allowance to $15 per dependent in 2008 and thus declined federal funding that had been offered as part of the Unemployment Insurance Modernization Act. Given that $15 per week (or $60 per month) for each child or other dependent would go much further to help families struggling with unemployment than the current allowance level, Michigan’s Legislature should raise the dependents’ allowance accordingly even in the absence of the federal incentive. This would be especially helpful in light of the failure by the Legislature to update the basic weekly benefit.

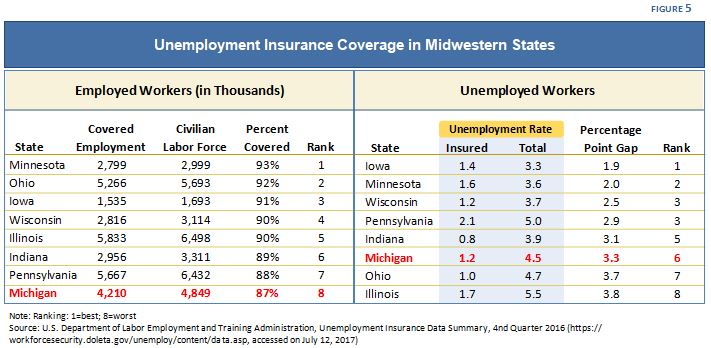

MICHIGAN HAS THE LOWEST UNEMPLOYMENT INSURANCE COVERAGE IN THE MIDWEST

Covered employment is defined as the number of employees who are covered by the UI system should they become unemployed, as reported to the state UI agency by employers. As a percent of the total labor force, Michigan’s covered employment during the fourth quarter of 2016 improved significantly since the 2012 edition of this paper, but remains the lowest in the Midwest (though not by far), while Minnesota’s is the highest at 93% (Figure 5).

When comparing Michigan’s Insured Unemployment Rate (1.2) against its Total Unemployment Rate (4.5), the state has a gap of 3.3 percentage points, placing it sixth out of the eight Midwestern states. This is an improvement over the 2012 version of this report when its gap was worst in the Midwest at 7.2 percentage points.9

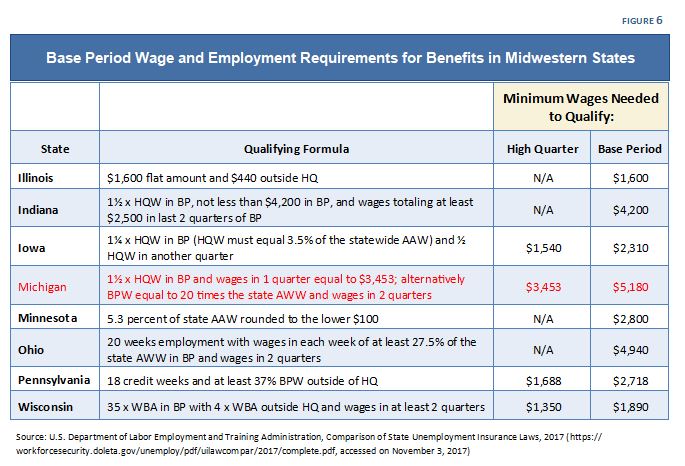

Michigan’s lower UI coverage relative to the rest of the Midwest may be due in part to the higher base period and high quarter wage eligibility levels. The base period is the time period during which wages determine eligibility for UI benefits, usually the first four of the last five completed calendar quarters preceding the filing of the claim.10 The high quarter is the quarter with the highest earnings within the base period.

Because each state uses its own qualifying formula to determine eligibility, it is difficult to do a straightforward comparison of eligibility requirements. However, when Michigan’s minimum wages for eligibility during the base period and high quarter are compared to those of its Midwestern peers, it is clear that Michigan’s UI program eligibility is much more restrictive than most of the others. While five of its peer states have base period minimums lower than $3,000, Michigan has the highest in the Midwest with $5,180. Of the four peer states with high quarter wage minimums, Michigan’s is $3,453 while the other three have minimums below $2,700 (Figure 6).

MICHIGAN SPENDS LESS ON UI PER UNEMPLOYED WORKER THAN MOST MIDWESTERN STATES

One way to compare the overall responsiveness of state UI programs is to calculate the amount of UI benefit dollars spent per unemployed worker in each state, taking into account all unemployed workers and not just those covered by UI. In 2010, Michigan was last among the eight Midwestern states in this measure (even with federal long-term UI funds included), but in 2016 was sixth out of eight, spending $299 per unemployed worker. While this is an improvement compared to peer states, Michigan spends considerably less than Minnesota, Iowa, Pennsylvania and Illinois, which pay more than $100 more per worker than Michigan (Figure 7). Minnesota and Illinois pay nearly $300 more per worker than Michigan.

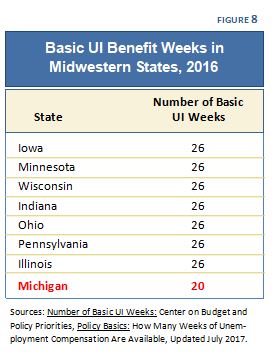

MICHIGAN ALLOWS THE FEWEST WEEKS OF UI BENEFITS IN THE MIDWEST

In 2011, despite having one of the highest unemployment rates in the nation and having been hit especially hard by the economic downturn, Michigan’s Legislature voted to make Michigan the first state to reduce the maximum number of weeks of Basic UI from 26 weeks to 20 weeks. This change took effect in January 2012. No other Midwest state has reduced its benefit weeks this drastically; the one other Midwest state to reduce its weeks, Illinois, shaved off only one week but restored the maximum to 26 a couple years later (Figure 8).

In 2011, despite having one of the highest unemployment rates in the nation and having been hit especially hard by the economic downturn, Michigan’s Legislature voted to make Michigan the first state to reduce the maximum number of weeks of Basic UI from 26 weeks to 20 weeks. This change took effect in January 2012. No other Midwest state has reduced its benefit weeks this drastically; the one other Midwest state to reduce its weeks, Illinois, shaved off only one week but restored the maximum to 26 a couple years later (Figure 8).

On this indicator, as with so many others, Michigan’s policies have put the state last in the Midwest. While many workers receiving UI find work before reaching the maximum number of weeks, it is important that Michigan restore the 26-week maximum, especially for workers in areas with few jobs.

MICHIGAN’S FRAUD DETERMINATION SYSTEM HAS VICTIMIZED TENS OF THOUSANDS OF UI RECIPIENTS

Beginning in 2013, workers who became unemployed began filing claims using Michigan’s new online unemployment system, called the Michigan Integrated Data Automated System (MiDAS). In ensuing years many workers received notices in the mail, in some cases long after they had found work and stopped receiving UI benefits, informing them that the UI benefits they received were fraudulent and that they owed thousands of dollars in benefit repayment plus interest and large penalties. The notices did not provide information as to the reason for the fraud determination.

While some workers were able to respond to their first notification in a timely manner and resolve the problem, many did not receive that notification because it was sent to an old address, or sent through online UI accounts that they no longer checked after they stopped receiving benefits. By the time these workers received a subsequent notification, they had passed the 30-day period in which they could contest or appeal the fraud determinations. Many began paying what the government said they owed, while others had wages and tax refunds garnished. Some workers filed for bankruptcy or experienced home foreclosure.

An internal investigation by the Michigan Unemployment Insurance Agency showed that more than 37,000 determinations of fraud by the Unemployment Insurance Agency since 2013 were wrongly determined (false) and that there had been in fact no fraud committed in those cases. Of the cases in which the fraud determination had been done entirely by computer, without human involvement, 93% were false determinations. Of the cases in which there was human as well as computer involvement, just under half were false, underscoring that while the computer system played a major role, there were structural problems and not just technical problems that contributed to the false fraud determinations.

The structural problems spanned the full range of the process:

- Determination—Fraud determinations were often triggered by small mistakes or by inconsistencies that were not the fault of the claimant.

- Notification—Notifications to the claimant of the fraud determination were often sent out more than a year after the claimant stopped receiving benefits, sometimes to an old mailing address or to an online UI account that the claimant had stopped checking due to having found employment. Many claimants found out about the determinations long after the 30-day response period had ended.

- Claimant Ability to Respond—The questionnaire provided to claimants who wanted to contest the false fraud findings against them included questions and answer choices that were unclear and self-incriminating.

- Recoupment—Many claimants unexpectedly had large portions of wages or tax refunds garnished, leaving little money left to pay for living expenses.

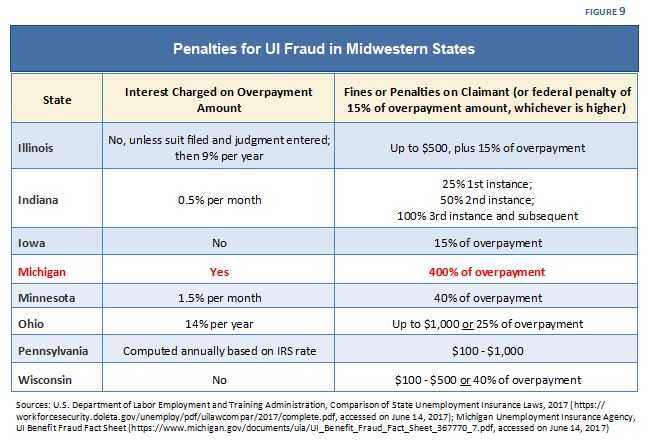

- Penalties—The federal requirement is that states have a penalty of at least 15% of the amount overpaid, but states can implement higher penalties if they choose. At 400% of the amount overpaid, Michigan had the harshest fraud penalties in the nation, and by far the harshest in the Midwest (Figure 9). Those falsely accused of fraud were told they owed the amount ostensibly overpaid, plus four times that amount, plus interest.

Michigan has recently enacted legislation to undertake serious reform on how fraud is determined and addressed, including:

- Requiring the UI agency to provide advocacy services for claimants who believe they have been wrongly determined;

- Prohibiting the agency from charging interest for at least one year after the fraud determination;

- Clarifying and strengthening the penalties for stealing another worker’s identity in order to receive UI benefits in their name and for failure of an employer to provide adequate or timely information to the UI agency about an employee’s unemployment status (two factors leading to some of the false fraud determinations);

- Providing hardship waivers from collection of overpaid funds;

- Making it easier for individuals accused of fraud to show good cause (i.e., the notice was sent by the UI agency to the wrong address) in not responding within the 30-day period; and

- Reducing fraud penalties to 100% of the amount overpaid for the first violation and 150% for subsequent violations (penalties for identity theft would remain at 400%).

ONE RECENT POLICY IMPROVENT: WORK SHARING

In 2012, Michigan became the 24th state to adopt a UI work-sharing program (there are now 28 states with a program), which in Michigan is called Work Share. The program provides an alternative to layoffs for businesses that need to reduce their payroll hours due to decreased demand for their products or services, allowing qualifying employers to reduce the payroll hours of a large pool of employees by an equal amount (usually 15%-40%) rather than eliminate some workers altogether. The employer informs the state UI agency of the percentage of payroll hours that will be reduced, and upon approval from the agency, each employee would be eligible for a proportional percentage of the UI benefits he or she would receive if laid off entirely.

Employers must provide assurance that during the work-sharing period they will not hire or transfer employees into the affected work unit, will not lay off or further reduce the hours of participating employees, and have attained the approval of the collective bargaining representative if the workforce is unionized. Participating in work sharing does not count against a worker’s available weeks of Unemployment Insurance, nor is the employee required to participate in job search activities since it is expected that he or she will eventually work full time again for the employer.

Workers benefit from work sharing because they will have less disruption in their household income than if they were laid off, and will continue receiving health insurance and other benefits without interruption (this is a requirement of the law). Employers benefit from work sharing because being able to retain their skilled workers rather than having to search for, hire and train new workers when business improves reduces unpredictability and costs.

WHAT DECISIONS HAVE LED TO MICHIGAN’S UI PROGRAM COMPARING SO POORLY TO PEER STATES?

- The decoupling of benefit levels from average weekly wages in 1994. While the maximum benefit had been set as a percentage (58%) of the average weekly wage prior to 1994, it was changed that year to a flat rate that erodes each year compared with wages unless increased by the Legislature. It has only been increased once since 1995 and is now equal to only 39% of the average weekly wage.

- An eligibility system that makes it difficult for workers to be eligible for UI. While Illinois, Iowa, Minnesota, Pennsylvania and Wisconsin allow some workers to collect benefits with base period earnings as low as $1,600-$2,800, Michigan’s minimum is $5,180. Likewise, Michigan’s high quarter minimum wage requirement is $3,453—more than $1,700 higher than other Midwest states with a high quarter requirement for eligibility.

- Failure to modernize the UI system in 2008 despite federal funding of much of the costs. Under the Unemployment Insurance Modernization Act of 2008, Michigan had the opportunity to receive federal funding to cover a significant portion of the costs of making at least two modernizations to its eligibility and benefit rules. Such updates included making UI available to those looking only for part-time work, those participating in skills training instead of job search, and/or those who left work for compelling family reasons such as spouse relocation, caring for an ill or disabled family member, or domestic violence. Increasing Michigan’s dependent allowance from $6 to $15 per dependent would have also counted as one modernization. While four other Midwestern states (and 33 states nationally) modernized their systems before the August 2011 deadline and thus became eligible for the funding, Michigan opted to do nothing and leave the money on the table.

- A reduction in 2011 to the number of weeks of UI available to workers. Despite having had some of the worst unemployment in the country, Michigan became the first state to reduce its maximum number of available UI weeks from 26 to 20.

RECOMMENDATIONS

These four indicators show that Michigan, despite having one of the higher unemployment rates in the Midwest, has the least responsive Unemployment Insurance system. This is bad for not only workers and their families, but for local economies and small businesses as well. Following are recommendations that would help Michigan’s UI system to more adequately respond to economic downturns in the state.

- First, do no harm. As the Legislature considers further UI legislation, it should take into account whether such legislation will strengthen Michigan’s UI program and bring it in line with other states or cause it to fall further behind in responding to the needs of workers. Michigan’s Legislature should say no to any legislation that will make it more difficult for unemployed workers to access UI as they look for work.

- Restore the 26-week maximum for Basic UI. Just as it took legislative action to reduce the maximum number of weeks for UI from 26 to 20, it will take legislative action to reverse this action. The Legislature can continue being “penny wise and pound foolish” and letting job providers lose money through reduced customer revenue as unemployed workers exhaust their benefits. Or, it can help workers, their families and job providers by restoring the 26-week maximum and providing a safety net for those who remain unable, despite their efforts, to secure employment after 20 weeks of job search.

- Peg the maximum benefit to the average weekly wage. Until 1994 the maximum benefit was set at 58% of the average weekly wage. Unlike the flat rate currently in use, pegging the maximum benefit to wages enables it to keep pace with economic realities without the need for periodic legislative adjustments. As the average wage increases, the maximum benefit increases accordingly; when the average wage falls, as it did in 2009 and 2010, the maximum benefit also falls. When determining the percentage, keep in mind the advisory council recommendation that the maximum benefit equal two-thirds of the average weekly wage. Although Michigan’s 58% standard fell short of this recommendation, it would have enabled a more generous maximum in recent years than the flat rate of $362 currently in place.

- Lower the minimum base period and high quarter earnings requirements for unemployed workers to collect UI benefits. Many workers who are firmly attached to the labor force do not qualify for UI because their earnings when employed were not high enough. Revisiting and adjusting these minimums will allow more workers to collect benefits as they look for work.

- Expand eligibility for UI to unemployed workers seeking part-time work, workers who left their jobs out of necessity for compelling family reasons, and/or workers who became unemployed and are using their time to acquire new skills through training rather than looking for immediate employment. Each of these eligibility expansions were options under the Unemployment Insurance Modernization Act that would have enabled Michigan to receive federal funding. While the federal money is no longer available, Michigan can still undertake one or more of these eligibility expansions for the good of its workers and its local economies.

- Raise the dependents’ allowance from $6 to $15. This was also an option that would have allowed Michigan to receive funding under the Unemployment Insurance Modernization Act. Increased benefits due to a larger dependents’ allowance would still be subject to the current $362 weekly maximum benefit level, so this would ideally be done in tandem with an increase in the maximum benefit.

Unemployment Insurance is good for the economy. When consumer spending is interrupted by high unemployment, businesses suffer. UI keeps consumer dollars flowing into local businesses such as retail stores, automobile service shops, home repair contractors, gas stations and hair salons. Economic analysis has shown that for every one dollar of unemployment benefits provided during the Great Recession, two dollars were added to the nation’s gross domestic product.11

Likewise, Unemployment Insurance helps workers and their families preserve their way of life and avoid serious economic hardship as they look for work. Allowing more workers, particularly workers with lower earnings, to access UI would enable many more families to weather a period of unemployment without major disruption, and raising benefits would result in UI better helping families keep up with expenses and bills. Strengthening Michigan’s system is the right thing to do.

ENDNOTES:

- Advisory Council on Unemployment Compensation, Collected Findings and Recommendations 1994-1996, Reprinted from Annual Reports of the Advisory Council on Unemployment Compensation to the President and Congress, 1996. (https://workforcesecurity.doleta.gov/dmstree/misc_papers/advisory/acuc/collected_findings/adv_council_94-96.pdf, accessed on January 8, 2018.)

- O’Leary, C. J., The Adequacy of Unemployment Insurance Benefits, W. E. Upjohn Institute for Employment Research, 1995.

- Evangelist, M. and R. McHugh, Coming Back for More: Michigan Lawmakers Aim to Cut Unemployment Insurance for Second Time in Six Months, National Employment Law Project, September 2011.

- Working Poor Families Project data generated by the Population Reference Bureau from the American Community Survey, 2015.

- Ibid.

- Halsey, O. S., Bulletin: Dependents’ Allowances Under State Unemployment Insurance Laws, Social Security Administration, February 1951. (https://www.ssa.gov/policy/docs/ssb/v14n2/v14n2p3.pdf, accessed on November 12, 2017.)

- Bulletin: State Unemployment Insurance Legislation, 1951, Social Security Administration, December, 1951. (https://www.ssa.gov/policy/docs/ssb/v14n12/v14n12p11.pdf, accessed on November 12, 2017.)

- Calculated using the Consumer Price Index Inflation Calculator of the Bureau of Labor Statistics.

- The Insured Unemployment Rate is computed by dividing the number of insured unemployed workers for the current quarter by the number of workers in “covered employment” for the first four of the last six completed quarters. The Total Unemployment Rate refers to the seasonally adjusted unemployment rate that is computed by dividing the number of unemployed workers by the total number of workers in the labor force. (U.S. Department of Labor Employment and Training Agency).

- Michigan and some other states (including all of the peer states compared in this report) use an alternative or expanded base period for workers who fail to qualify under the regular base period. In Michigan and some other states, if a worker fails to qualify using wages and employment in the first four of the five most recent completed calendar quarters, the state will use wages and employment in the most recent four completed calendar quarters.

- Boushey, H. and J. Eizenga, Toward a Strong Unemployment Insurance System: The Case for an Expanded Federal Role, Center for American Progress, February 2011.

Betsy Zobl-Tar

Betsy Zobl-Tar  Jay Cutler joined the League in March 2026 as the Kids Count Senior Data Analyst, where he collects, analyzes, and prepares data for Kids Count in Michigan.

Jay Cutler joined the League in March 2026 as the Kids Count Senior Data Analyst, where he collects, analyzes, and prepares data for Kids Count in Michigan. Danielle Taylor-Basemore joined the League as the Development Data and Stewardship Coordinator in June 2025. She brings with her five years of nonprofit experience with a special focus on community engagement, data visualization and strategic programming. Prior to joining the League, Danielle served as the Business District, Safety, and Digital Manager at Jefferson East, Inc.

Danielle Taylor-Basemore joined the League as the Development Data and Stewardship Coordinator in June 2025. She brings with her five years of nonprofit experience with a special focus on community engagement, data visualization and strategic programming. Prior to joining the League, Danielle served as the Business District, Safety, and Digital Manager at Jefferson East, Inc. Scott Preston is a Senior Policy Analyst with the Michigan League for Public Policy, where he leads the organization’s immigration and criminal justice reform portfolios. In the three years prior to joining the League, Scott facilitated the Southeast Michigan Refugee Collaborative and managed a small business economic development program at Global Detroit. His work included launching Michigan’s first Refugee Film Festival and building on a trusted connector model that linked marginalized communities with crucial resources. Scott’s work at the League is informed by his background in journalism and research. He spent four years covering the Syrian refugee crisis in the Middle East for publications such as The Economist, and later worked with unaccompanied refugee minors through Samaritas. Scott holds a master’s degree in international migration and public policy from the London School of Economics and Political Science.

Scott Preston is a Senior Policy Analyst with the Michigan League for Public Policy, where he leads the organization’s immigration and criminal justice reform portfolios. In the three years prior to joining the League, Scott facilitated the Southeast Michigan Refugee Collaborative and managed a small business economic development program at Global Detroit. His work included launching Michigan’s first Refugee Film Festival and building on a trusted connector model that linked marginalized communities with crucial resources. Scott’s work at the League is informed by his background in journalism and research. He spent four years covering the Syrian refugee crisis in the Middle East for publications such as The Economist, and later worked with unaccompanied refugee minors through Samaritas. Scott holds a master’s degree in international migration and public policy from the London School of Economics and Political Science. Kate Powers joined the League as the Chief Development Officer in February 2025. Prior to joining the League, Kate held leadership positions at many Michigan nonprofit organizations, most recently serving as the COO and Chief Development Officer of Ele’s Place. Kate has spent the bulk of her career in fundraising, with a short stint in the state Legislature as a legislative aide to members in both chambers. Kate is a graduate of Michigan State University’s James Madison College with a Bachelor of Arts in Social Relations and has a certificate in fundraising management from the Lilly Family School of Philanthropy at Indiana University. Additionally, Kate served on the East Lansing Public Schools Board of Education and is a past President of the Junior League of Lansing. In her free time, she enjoys traveling with her husband and her son and saving outfit of the day and home decor ideas on Pinterest.

Kate Powers joined the League as the Chief Development Officer in February 2025. Prior to joining the League, Kate held leadership positions at many Michigan nonprofit organizations, most recently serving as the COO and Chief Development Officer of Ele’s Place. Kate has spent the bulk of her career in fundraising, with a short stint in the state Legislature as a legislative aide to members in both chambers. Kate is a graduate of Michigan State University’s James Madison College with a Bachelor of Arts in Social Relations and has a certificate in fundraising management from the Lilly Family School of Philanthropy at Indiana University. Additionally, Kate served on the East Lansing Public Schools Board of Education and is a past President of the Junior League of Lansing. In her free time, she enjoys traveling with her husband and her son and saving outfit of the day and home decor ideas on Pinterest.  Nicholas Hess joined the League as the Fiscal Policy Analyst in September of 2024. In this role, Nicholas focuses on tax policy, government revenue, and their impact on working families and racial equity, including the effects of the Earned Income Tax Credit (EITC) and Child Tax Credit (CTC). Nicholas values the role that judicious fiscal policy can play in the improvement of people’s lives and the economy, alleviating inequities along the way.

Nicholas Hess joined the League as the Fiscal Policy Analyst in September of 2024. In this role, Nicholas focuses on tax policy, government revenue, and their impact on working families and racial equity, including the effects of the Earned Income Tax Credit (EITC) and Child Tax Credit (CTC). Nicholas values the role that judicious fiscal policy can play in the improvement of people’s lives and the economy, alleviating inequities along the way. Audrey Matusz joined the League as the Visual Communications Specialist in September 2024. She supports the team with implementing social media strategies and brainstorming creative ways to talk about public policy. She brings with her nearly a decade of experience in producing digital products for evidence-based social justice initiatives.

Audrey Matusz joined the League as the Visual Communications Specialist in September 2024. She supports the team with implementing social media strategies and brainstorming creative ways to talk about public policy. She brings with her nearly a decade of experience in producing digital products for evidence-based social justice initiatives.  Jacob Kaplan

Jacob Kaplan  Donald Stuckey

Donald Stuckey  Alexandra Stamm

Alexandra Stamm

Amari Fuller

Amari Fuller Mikell Frey is a communications professional with a passion for using the art of storytelling to positively impact lives. She strongly believes that positive social change can be inspired by the sharing of data-driven information coupled with the unique perspectives of people from all walks of life across Michigan, especially those who have faced extraordinary barriers.

Mikell Frey is a communications professional with a passion for using the art of storytelling to positively impact lives. She strongly believes that positive social change can be inspired by the sharing of data-driven information coupled with the unique perspectives of people from all walks of life across Michigan, especially those who have faced extraordinary barriers.

Yona Isaacs (she/hers) is an Early Childhood Data Analyst for the Kids Count project. After earning her Bachelor of Science in Biopsychology, Cognition, and Neuroscience at the University of Michigan, she began her career as a research coordinator in pediatric psychiatry using data to understand the impacts of brain activity and genetics on children’s behavior and mental health symptoms. This work prompted an interest in exploring social determinants of health and the role of policy in promoting equitable opportunities for all children, families, and communities. She returned to the University of Michigan to complete her Masters in Social Work focused on Social Policy and Evaluation, during which she interned with the ACLU of Michigan’s policy and legislative team and assisted local nonprofit organizations in creating data and evaluation metrics. She currently serves as a coordinator for the Michigan Center for Youth Justice on a project aiming to increase placement options and enhance cultural competency within the juvenile justice system for LGBTQIA+ youth. Yona is eager to put her data skills to work at the League in support of data-driven policies that advocate for equitable access to healthcare, education, economic security, and opportunity for 0-5 year old children. In her free time, she enjoys tackling DIY house projects and trying new outdoor activities with her dog.

Yona Isaacs (she/hers) is an Early Childhood Data Analyst for the Kids Count project. After earning her Bachelor of Science in Biopsychology, Cognition, and Neuroscience at the University of Michigan, she began her career as a research coordinator in pediatric psychiatry using data to understand the impacts of brain activity and genetics on children’s behavior and mental health symptoms. This work prompted an interest in exploring social determinants of health and the role of policy in promoting equitable opportunities for all children, families, and communities. She returned to the University of Michigan to complete her Masters in Social Work focused on Social Policy and Evaluation, during which she interned with the ACLU of Michigan’s policy and legislative team and assisted local nonprofit organizations in creating data and evaluation metrics. She currently serves as a coordinator for the Michigan Center for Youth Justice on a project aiming to increase placement options and enhance cultural competency within the juvenile justice system for LGBTQIA+ youth. Yona is eager to put her data skills to work at the League in support of data-driven policies that advocate for equitable access to healthcare, education, economic security, and opportunity for 0-5 year old children. In her free time, she enjoys tackling DIY house projects and trying new outdoor activities with her dog. Rachel Richards rejoined the League in December 2020 as the Fiscal Policy Director working on state budget and tax policies. Prior to returning to the League, she served as the Director of Legislative Affairs for the Michigan Department of Treasury, the tax policy analyst and Legislative Director for the Michigan League for Public Policy, and a policy analyst and the Appropriations Coordinator for the Democratic Caucus of the Michigan House of Representatives. She brings with her over a decade of experience in policies focused on economic opportunity, including workforce issues, tax, and state budget.

Rachel Richards rejoined the League in December 2020 as the Fiscal Policy Director working on state budget and tax policies. Prior to returning to the League, she served as the Director of Legislative Affairs for the Michigan Department of Treasury, the tax policy analyst and Legislative Director for the Michigan League for Public Policy, and a policy analyst and the Appropriations Coordinator for the Democratic Caucus of the Michigan House of Representatives. She brings with her over a decade of experience in policies focused on economic opportunity, including workforce issues, tax, and state budget. Simon Marshall-Shah joined the Michigan League for Public Policy as a State Policy Fellow in August 2019. His work focuses on state policy as it relates to the budget, immigration, health care and other League policy priorities. Before joining the League, he worked in Washington, D.C. at the Association for Community Affiliated Plans (ACAP), providing federal policy and advocacy support to nonprofit, Medicaid health plans (Safety Net Health Plans) related to the ACA Marketplaces as well as Quality & Operations.

Simon Marshall-Shah joined the Michigan League for Public Policy as a State Policy Fellow in August 2019. His work focuses on state policy as it relates to the budget, immigration, health care and other League policy priorities. Before joining the League, he worked in Washington, D.C. at the Association for Community Affiliated Plans (ACAP), providing federal policy and advocacy support to nonprofit, Medicaid health plans (Safety Net Health Plans) related to the ACA Marketplaces as well as Quality & Operations.

Renell Weathers, Michigan League for Public Policy (MLPP) Community Engagement Consultant. As community engagement consultant, Renell works with organizations throughout the state in connecting the impact of budget and tax policies to their communities. She is motivated by the belief that all children and adults deserve the opportunity to achieve their dreams regardless of race, ethnicity, religion or economic class.

Renell Weathers, Michigan League for Public Policy (MLPP) Community Engagement Consultant. As community engagement consultant, Renell works with organizations throughout the state in connecting the impact of budget and tax policies to their communities. She is motivated by the belief that all children and adults deserve the opportunity to achieve their dreams regardless of race, ethnicity, religion or economic class.

Emily Jorgensen joined the Michigan League for Public Policy in July 2019. She deeply cares about the well-being of individuals and families and has a great love for Michigan. She is grateful that her position at the League enables her to combine these passions and work to help promote policies that will lead to better opportunities and security for all Michiganders.

Emily Jorgensen joined the Michigan League for Public Policy in July 2019. She deeply cares about the well-being of individuals and families and has a great love for Michigan. She is grateful that her position at the League enables her to combine these passions and work to help promote policies that will lead to better opportunities and security for all Michiganders.

Megan Farnsworth joined the League’s staff in December 2022 as Executive Assistant. Megan is driven by work that is personally fulfilling, and feels honored to help support the work of an organization that pushes for more robust programming and opportunities for the residents of our state. She’s excited and motivated to gain overarching knowledge of the policies and agendas that the League supports.

Megan Farnsworth joined the League’s staff in December 2022 as Executive Assistant. Megan is driven by work that is personally fulfilling, and feels honored to help support the work of an organization that pushes for more robust programming and opportunities for the residents of our state. She’s excited and motivated to gain overarching knowledge of the policies and agendas that the League supports.

{kind=link}